By Rick Schreiber, Chai Hoang and Chris Bard

Last year, over 6,000 manufacturers claimed more than an estimated $10 billion in research tax credits (RTCs), with each manufacturer’s average benefit exceeding $1 million.

Generated in part by manufacturers’ efforts to develop new and improved products and processes, these benefits were also generated by their continued investment to develop or improve software to manage or automate production processes and business intelligence, among other things.

This year, thanks to new regulations that broaden the range of software development activities eligible for the credit, more manufacturers may be able to take even greater advantage of these dollar-for-dollar offsets against tax liability, enabling them to invest more in new technologies, expand their labor force and finance other business objectives.

RTC Explained

Often also called the “R&D credit,” the research tax credit is an activities-based credit. Federal and state RTCs are available, in general, to businesses that attempt to develop or improve the functionality or performance of a product, process, software or other component using engineering, physics, biology or the computer sciences to evaluate alternatives and eliminate uncertainty regarding the business’ capability or method to develop or improve the component or the component’s appropriate design (Qualified Research).

RTCs equal to up to an average of 10 percent of qualified spending, which generally includes taxable wage, supply, contractor and cloud-computing expenses related to these attempts. More than 6,000 manufacturers reported performing qualified activities last year, and a recent BDO/MPI Survey shows that this number could be double that.

More than a majority (57 percent) of survey respondents said they weren’t planning to claim tax incentives like the RTC, even though they were planning to do development work to leverage the Internet of Things to capture and communicate more data more accurately and reliably.

This type of work likely qualifies for the RTC, but many respondents said they weren’t going to claim it because they thought they lacked sufficient documentation or weren’t performing qualified activities.

Happily, these aren’t good reasons not to claim the RTC: several court cases have affirmed that oral testimony can be used to claim and support RTCs; and any manufacturer trying to make something better, faster, cheaper or greener is likely to be performing qualified activities, whether the activities succeed or not.

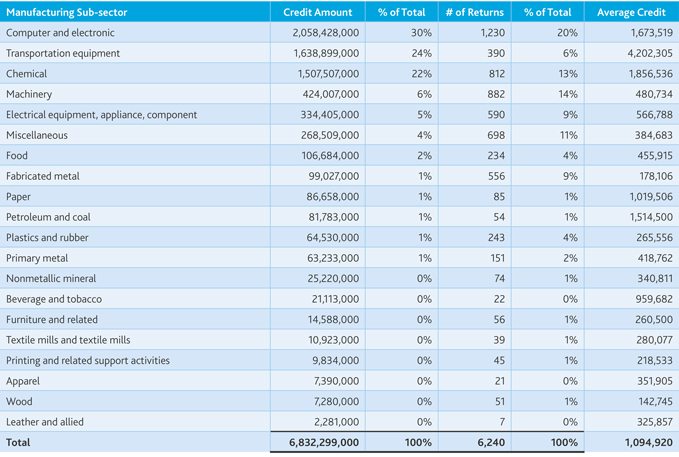

To that point, manufacturers in the following sub-sectors reported RTCs in 2013, the latest year for which IRS statistics are available:

And although many of these credits related to attempts to design and develop new products and processes, many also related to efforts to develop new or improved software.

Software Development RTC Opportunity Expanded

New final Treasury Regulations issued in October will increase the RTCs manufacturers claim for software development.

Under current and former rules, software development activities fall into two categories, depending on whether the software being developed is intended primarily for the taxpayer’s internal use or not. What category the software falls into is important because “internal use software” (IUS) development activities must meet a higher standard to qualify than activities to develop non-IUS software.

The Final Regulations narrow the definition of IUS considerably. This means that considerably more software development activities are eligible for the credit, which means that more manufacturers may claim more RTCs going forward.

IUS is software developed for use in general and administrative (G&A) back-office functions that facilitate or support the conduct of the company’s trade or business. G&A functions are defined as financial management functions, human resource management functions and support services functions.

Whether software is IUS depends upon whether the taxpayer, at the beginning of development, intended the software to be used primarily for G&A purposes. Software is not IUS if it is developed to enable a taxpayer to interact with third parties or to allow third parties to initiate functions or review data on the taxpayer’s system.

IUS development may also qualify. The regulations also provide that Qualified Research to develop IUS qualifies if it:

- Is intended to develop software that would be innovative, i.e., result in a reduction in cost, improvement in speed or other measurable improvement that is substantial and economically significant;

- Involves significant economic risk, as where the taxpayer commits substantial resources to the development and there is substantial uncertainty, because of technical risk, that such resources would be recovered within a reasonable period. The focus should be on the level of uncertainty and not the type of uncertainty; and

- Is intended to develop software that isn’t commercially available for use by the taxpayer without modifications that would satisfy the first two requirements.

Manufacturers and the RTC Tax Credit

The new regulations apply to a vast array of manufacturers’ activities, and businesses in this space should consider whether they’re missing out on opportunities to benefit from the RTC. Manufacturers have undertaken an effort to digitalize their operations, supply chains and markets.

Companies are increasingly engaged in the development and improvement of business-intelligence software systems and enterprise-resource-management tools. The development, optimization and integration of the Internet of Things to enhance manufacturing and related processes also often qualify for RTCs.

Additionally, sales and operations planning require data from all aspects of a business, from production throughput and distribution and warehousing to financial metrics.

The development and implementation of software to monitor and manage back-office functions could qualify for the RTC, e.g. activities to develop software related to:

- Supply chain functionality;

- Forecasting based on historical baselines, promotions and sales;

- Pricing optimization, of both sales to consumers and procurement of supplies;

- Inventory management;

- Order management;

- Revenue management;

- Routing engineering/software development; and

- Security against cyber-attacks.

Because the final regulations exclude from the definition of IUS software that is developed to enable a taxpayer to interact with third parties or to allow third parties to initiate functions or review data on the taxpayer’s system, manufacturers should review their software against the new definition and standards.

For example, software developed to manage supply orders, sales or production data with third parties, or to enable customers or third parties to track delivery of goods, search inventory, or receive services over the internet, may qualify under the new regulations, without having to meet the higher standards for IUS.

Conclusion

Manufacturers of all sizes have been benefitting from the RTC since its inception in 1981. Now, with the new regulations on software development, many more should be able to benefit more than ever before, thus reducing their taxes, freeing up capital and gaining a competitive advantage.

In addition, smaller manufacturers may be able to use the RTC against up to $250,000 of their payroll taxes or even their Alternative Minimum Tax.

Rick Schreiber is an Assurance & Advisory managing partner and the national leader of BDO’s Manufacturing & Distribution practice. He may be reached at rschreiber@bdo.com.

Chai Hoang is a manager in BDO’s Research and Development (R&D) Tax Services practice, and may be reached at choang@bdo.com.

Chris Bard is the practice leader for BDO’s Research and Development (R&D) Tax Services practice and chairman of BDO International’s Global R&D Center of Excellence. He may be reached at cbard@bdo.com.

This article originally appeared in BDO USA, LLP’s “Manufacturing Output” newsletter (Winter 2017). Copyright © 2017 BDO USA, LLP. All rights reserved.www.bdo.com