The Affordable Care Act (ACA) was enacted in 2010 as a way to reform health care in the United States. Employer mandates for providing health coverage go into effect between 2014 and 2018. Despite the fact that failing to meet ACA compliance deadlines can result in costly fines, many businesses seem ill-prepared to meet the compliance and reporting requirements imposed by the ACA.

The Affordable Care Act (ACA) was enacted in 2010 as a way to reform health care in the United States. Employer mandates for providing health coverage go into effect between 2014 and 2018. Despite the fact that failing to meet ACA compliance deadlines can result in costly fines, many businesses seem ill-prepared to meet the compliance and reporting requirements imposed by the ACA.

In order to operate in accordance with the law, and to avoid costly penalties, your organization must understand the ACA compliance deadlines and the steps necessary to become compliant.

2014 ACA Compliance Deadlines

- Small employers - those with less than 25 full-time equivalent employees - may qualify for tax credits for employer-sponsored healthcare. The credits can be for as much as 50 percent of what the employer pays toward health coverage.

- Incentives go into effect for organizations that provide employee wellness programs. Businesses can receive credits for up to 30 percent of their costs for providing the wellness program. If the program specifically addresses tobacco use, the credit amount can be as much as 50 percent of the employer’s contributions.

2015 ACA Compliance Deadlines

- Penalties for non-ACA compliance go into effect in 2015. These penalties only apply to organizations with 50 or more full-time equivalent employees. Businesses are required to offer both minimum essential coverage and a minimum value plans to eligible employees in order to avoid penalties. For 2015, 70 percent of eligible employees must be offered health coverage.

- Reporting requirements go into effect in 2015. Reporting must be submitted monthly with a summary provided at year end to the IRS and employees. Failing to file reports in a timely manner and in the correct format can result in fines.

2016 ACA Compliance Deadlines

- The threshold for offering employee coverage moves to its permanent levels. Beginning with the 2016 benefit year, health coverage must be offered to 95 percent of eligible full-time equivalent employees to avoid penalties.

2017 ACA Compliance Deadlines

- Beginning in 2017, large employers will be eligible to purchase health care coverage through health exchanges. Prior to this point, only small employers and individuals were able to take advantage of potential savings through the competition of the health care exchanges.

2018 ACA Compliance Deadlines

- The Excise Tax for employer sponsored health care coverage goes into effect in 2018. The government has established a threshold for the cost of health care coverage. The limit is $10,200 for individual plans or $27,500 for family plans. If the total cost, including both employer and employee cost, of coverage for a plan exceeds the limit, businesses must pay a tax of 40 percent of the excess.

- Many organizations believe that these predefined thresholds are so high that their organization is not likely to hit the ceiling. However, according to ADP, as many as 60 percent of employers have health care plans that will reach this limit – some as soon as 2018. For many organizations, the only way to avoid the excise tax will be to change the types of health coverage offered.

The Catastrophic Penalty

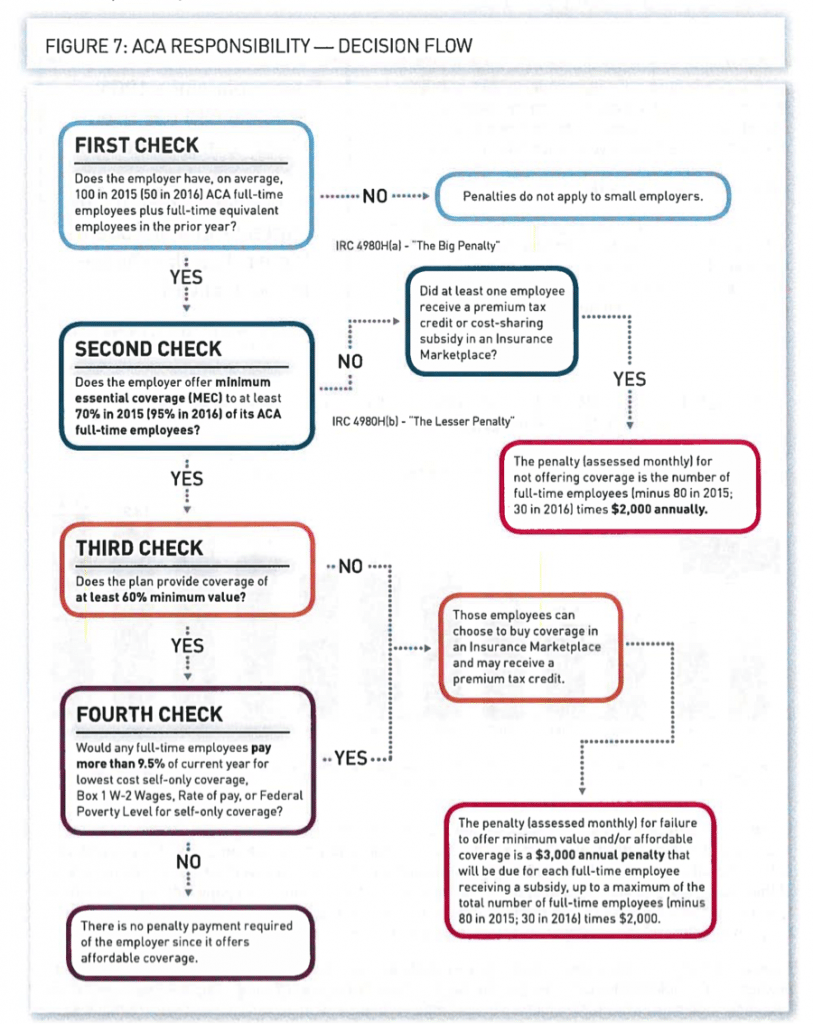

Also known as the “Big” penalty, this penalty is designed to enforce the mandate that employers offer minimum essential coverage plans to eligible employees. For the 2015 benefit year, large employers are required to offer health coverage to 70 percent of eligible employees. This threshold raises to 95 percent in 2016 and subsequent years. If an employer fails to meet this threshold, and one of the affected employees receives a federal subsidy in the federal healthcare exchange, the organization is subject to penalties. The catastrophic penalty is equal to $2,000 per year per FTE and applies to every employee. The penalty is assessed on a monthly basis.

The Individual Penalty

Alternatively referred to as the “lesser” penalty, this penalty evaluates an employer’s offering of a minimum value, affordable health plan. As opposed to the catastrophic penalty, which is based on the total number of FTEs, the individual penalty is levied only on those individuals who were not offered minimum value insurance, then were able to receive a federal subsidy through the health care exchanges. This penalty can be up to $3,000 per FTE that receives a subsidy, per year. In order to qualify as an affordable plan, the following guidelines must be met:

- The coverage must only cover the employee.

- The employee’s cost for the health plan can be no more than 9.5 percent of the employee’s wages, as reported in Box 1 on the W-2.

- The employee’s cost for the health plan can be no more than 9.5 percent of the federal poverty level as defined by the IRS.

- The employee’s cost for the health plan can be no more than 9.5 percent than 130 hours of their hourly wage at the beginning of the year.

The Individual Penalty was capped so that it cannot exceed the amount that would be due had the employer been subject to The Catastrophic Penalty.

ACA Responsibility – Decision Flow

It can be difficult to navigate the penalties assessed by the ACA. A full understanding of penalties and coverage requirements is necessary for an organization to make an informed decision about their coverage options, including deciding to not provide health coverage to employees. The following chart published by ADP can be helpful to determine what penalties, if any, your business is subject to, as well as the cost.

(Figure 7 provided by ADP)

Readying your organization to meet all ACA compliance deadlines can be difficult. To be done accurately, it is important that the implementation team has a thorough understanding of ACA guidelines and what steps are necessary for your organization to be compliant. The professional services of a qualified consultant can provide the support your organization needs to successfully meet ACA compliance deadlines.